Photo Credit: Kite rin / Shutterstock

Credit cards are a staple of the American financial system. Not only do they offer easy access to funds on short notice, but they serve as a foundational financial instrument for building up one’s credit score.

As of late, however, credit has been harder to come by for many consumers in the U.S. Rapidly rising inflation in 2021 and 2022 motivated the U.S. Federal Reserve to embark on a series of interest rate hikes that have continued into this year. As interest rates have risen, it has become more expensive for banks to borrow money.

Banks can respond to these constraints in several ways. Often, they simply pass on higher interest rates to consumers. But in many cases, the banks may also get choosier about issuing credit, whether by limiting how much they lend out or raising the standards for borrowers to get approved. This increased scrutiny can be felt across all lending products, from bank and vehicle loans, to consumer credit cards that many Americans rely on every day.

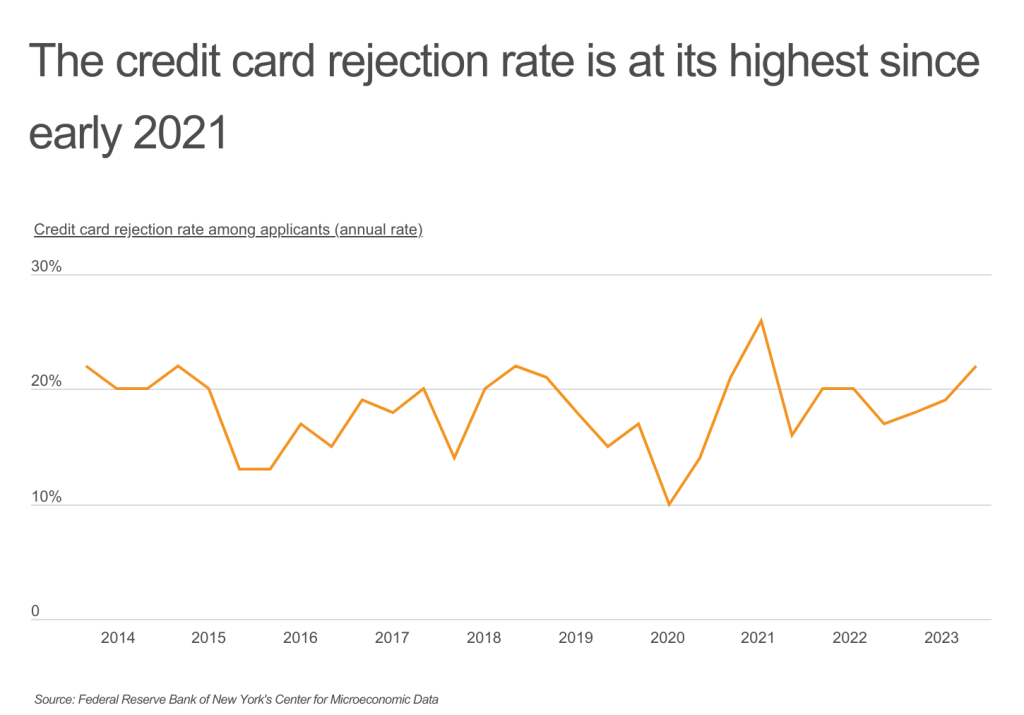

In this environment, more people’s credit card applications are being denied. The rejection rate for credit card applications as of June 2023 sits at 22%, one of the highest rates in a decade. After falling to a recent low of 10% in February 2020, the rejection rate spiked to 26% in just one year. Credit card rejection rates fell briefly in 2021 but have risen steadily over the last year.

Big-picture economic trends can certainly affect how likely a credit card application is to be approved, but credit card companies are also always looking at factors specific to each application when making an approval decision. Common reasons for rejection include low credit scores, high levels of debt, a history of late payments or bankruptcy, and insufficient income. But the biggest obstacle for many applicants is a “chicken or the egg” dilemma: it’s harder for someone to get approved for credit if they don’t already have a credit history.

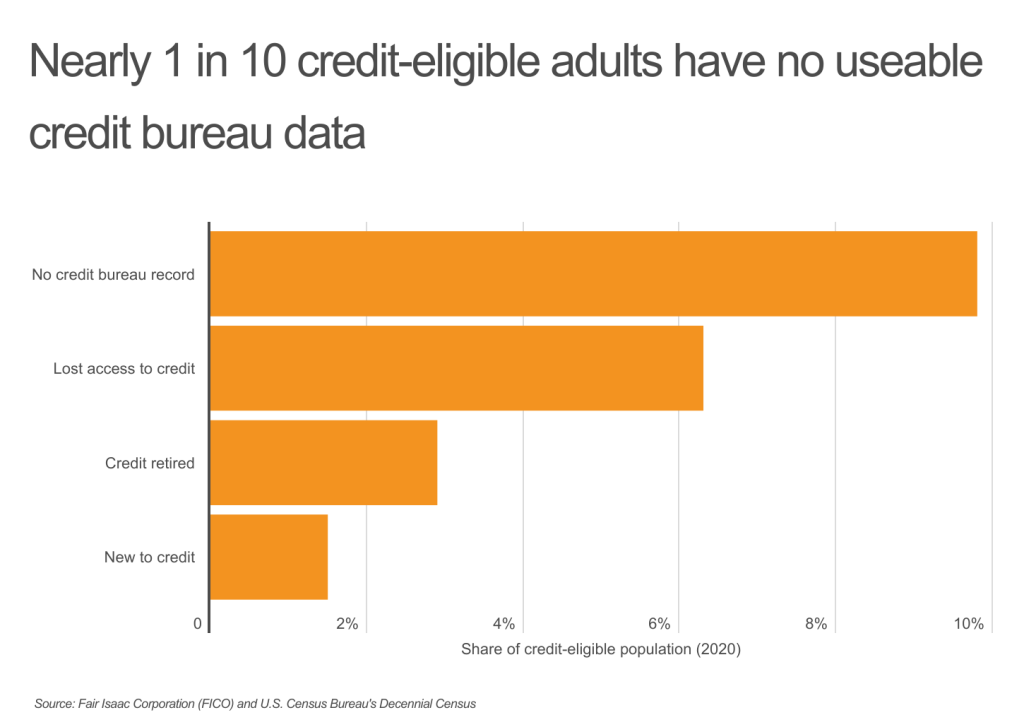

According to FICO, one of the leading credit scoring agencies in the U.S., nearly one in 10 credit-eligible adults—25.3 million out of 258 million—have no traditional credit bureau record. An additional 28 million adults have sparse credit files, whether because they are newer borrowers with limited history, older borrowers who have stopped using credit, or borrowers who have lost access to credit, most typically due to economic hardships.

While each of these groups can struggle to access credit cards and the financial benefits they can provide, those with no history at all are often at the greatest disadvantage. According to analysis from the Consumer Financial Protection Bureau, these “credit invisibles” are more likely to be Black or Hispanic or to come from a low-income area, factors that already face greater financial challenges.

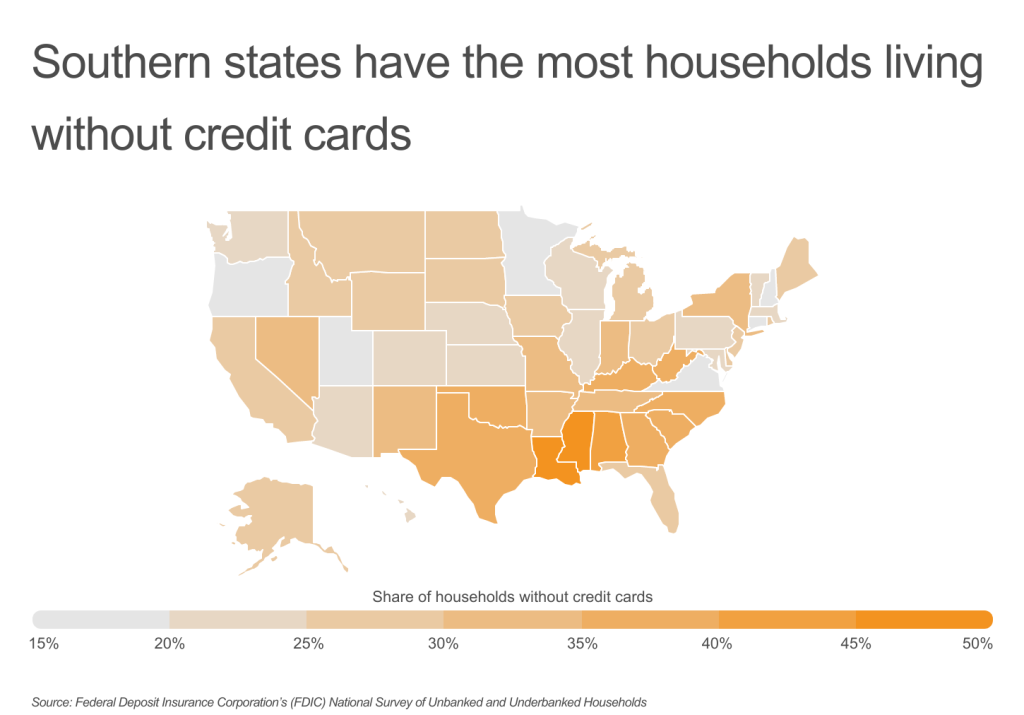

Given these demographic differences, certain parts of the country are more likely to lack credit cards. A total of 20 states have a higher share of households without credit cards than the national rate of 28.5%. Most of these states are found in the Southeast and Southwest, where incomes are lower and the Black and Hispanic populations tend to be higher. In some states, more than one in three households do not have access to a credit card, and in one state—Mississippi—over half (50.2%) of all households have no credit cards.

The data used in this analysis is from the Federal Deposit Insurance Corporation (FDIC). To determine the states where the most people lack credit cards, researchers at Upgraded Points calculated the share of households that did not possess any Visa, Mastercard, American Express, or Discover credit cards in the past 12 months. In the event of a tie, the state with the greater total households without credit cards was ranked higher.

Here are the states where the most people lack credit cards.

States Where the Most People Lack Credit Cards

Photo Credit: Mihai Andritoiu / Shutterstock

15. Indiana

- Share of households without credit cards: 31.4%

- Total households without credit cards: 865,384

- Share of households that are unbanked: 5.6%

- Share of households that are underbanked: 12.1%

Photo Credit: turtix / Shutterstock

14. New Mexico

- Share of households without credit cards: 31.9%

- Total households without credit cards: 282,315

- Share of households that are unbanked: 7.0%

- Share of households that are underbanked: 16.7%

Photo Credit: Sean Pavone / Shutterstock

13. Tennessee

- Share of households without credit cards: 33.4%

- Total households without credit cards: 966,262

- Share of households that are unbanked: 5.0%

- Share of households that are underbanked: 13.3%

Photo Credit: Andrey Bayda / Shutterstock

12. Nevada

- Share of households without credit cards: 33.5%

- Total households without credit cards: 420,090

- Share of households that are unbanked: 5.6%

- Share of households that are underbanked: 17.8%

Photo Credit: Sean Pavone / Shutterstock

11. Arkansas

- Share of households without credit cards: 33.6%

- Total households without credit cards: 429,408

- Share of households that are unbanked: 3.4%

- Share of households that are underbanked: 15.9%

Photo Credit: ESB Professional / Shutterstock

10. Georgia

- Share of households without credit cards: 35.1%

- Total households without credit cards: 1,515,618

- Share of households that are unbanked: 6.7%

- Share of households that are underbanked: 17.3%

Photo Credit: Sean Pavone / Shutterstock

9. Oklahoma

- Share of households without credit cards: 35.3%

- Total households without credit cards: 577,155

- Share of households that are unbanked: 5.4%

- Share of households that are underbanked: 20.5%

Photo Credit: Sean Pavone / Shutterstock

8. Texas

- Share of households without credit cards: 35.4%

- Total households without credit cards: 3,973,650

- Share of households that are unbanked: 5.6%

- Share of households that are underbanked: 18.4%

Photo Credit: Hendrickson Photography / Shutterstock

7. Kentucky

- Share of households without credit cards: 35.5%

- Total households without credit cards: 630,480

- Share of households that are unbanked: 5.2%

- Share of households that are underbanked: 16.1%

Photo Credit: Jon Bilous / Shutterstock

6. North Carolina

- Share of households without credit cards: 37.0%

- Total households without credit cards: 1,654,640

- Share of households that are unbanked: 3.3%

- Share of households that are underbanked: 13.9%

Photo Credit: Sean Pavone / Shutterstock

5. West Virginia

- Share of households without credit cards: 37.4%

- Total households without credit cards: 287,980

- Share of households that are unbanked: 3.0%

- Share of households that are underbanked: 12.4%

Photo Credit: Sean Pavone / Shutterstock

4. South Carolina

- Share of households without credit cards: 38.8%

- Total households without credit cards: 864,464

- Share of households that are unbanked: 5.5%

- Share of households that are underbanked: 16.1%

Photo Credit: Sean Pavone / Shutterstock

3. Alabama

- Share of households without credit cards: 43.5%

- Total households without credit cards: 889,575

- Share of households that are unbanked: 4.7%

- Share of households that are underbanked: 13.3%

Photo Credit: Sean Pavone / Shutterstock

2. Louisiana

- Share of households without credit cards: 47.6%

- Total households without credit cards: 892,976

- Share of households that are unbanked: 8.1%

- Share of households that are underbanked: 20.2%

Photo Credit: Sean Pavone / Shutterstock

1. Mississippi

- Share of households without credit cards: 50.2%

- Total households without credit cards: 599,890

- Share of households that are unbanked: 11.1%

- Share of households that are underbanked: 21.4%

Detailed Findings & Methodology

The data used in this analysis is from the 2021 Federal Deposit Insurance Corporation’s (FDIC) National Survey of Unbanked and Underbanked Households. To determine the states where the most people lack credit cards, researchers at Upgraded Points calculated the share of households that did not possess any Visa, MasterCard, American Express, or Discover credit cards in the past 12 months. In the event of a tie, the state with the greater total households without credit cards was ranked higher. Note, for the purposes of this analysis, unbanked households are those without a checking or savings bank account. Underbanked households were considered to be those households with a checking or savings bank account but who also relied on alternative financial services, such as: check cashing, money orders, international remittances, payday loans, rent-to-own services, pawn shop loans, refund anticipation loans, and auto title loans.

For complete results, see States Where the Most People Lack Credit Cards on Upgraded Points.